The Bank of England and HM Treasury begin work on a digital pound.

Earlier this week, the Bank of England (BoE) and HM Treasury announced that the joint Bank-HM Treasury CBDC Taskforce has begun preparatory work to issue a digital pound. Following the announcement, the BoE published a consultation paper and technology working paper to illustrate why and how a digital pound could be used. Additionally, the central bank provided data files that informed the CBDC Taskforce’s creation of the consultation and technology working papers. For background, the CBDC Taskforce was formed in April 2021 by Treasury Secretary Rishi Sunak, now the current Prime Minister.

The consultation paper provided many takeaways:

The digital pound would not replace cash but will reduce the amount in circulation.

The development roadmap indicates that issuance would occur no earlier than 2025.

There are concerns over bank disintermediation and subsequent short-term interest rate spikes due to a decline in bank reserves.

To prevent bank disintermediation, a £10,000-20,000 balance limit for individuals would be instituted.

CBDCs are viewed as a means to interdict the proliferation and adoption of non-sterling digital forms of money in the UK and abroad.

Demand for the digital pound would increase the BoE’s balance sheet over time.

The last takeaway implies second- and third-order effects for monetary policy that resemble quantitative easing. Demand for the digital pound switches commercial bank deposits to digital pounds, which forces banks to borrow more reserves in money markets. This would drive up short-term rates relative to the Bank Rate and force the BoE to increase the supply of reserves through its Short-Term Repo Facility to keep short-term rates close to Bank Rate. An increase in reserves would result in an increase in liabilities on the BoE’s balance sheet matched by an increase in assets, resulting in an overall increase in the size of the balance sheet.

Historically, growth in a central bank’s balance sheet stimulates an economy through additional liquidity and incentivizing borrowing / lending activity. However, the BoE anticipates a digital pound will generate only “small changes in the level of reserves.” The BoE remains confident that it would have “mitigants in place to manage these balance sheet changes.” Yet, it admits that the composition and size of the balance sheet, once the digital pound is introduced, are “highly uncertain.”

BTC and ETH experience golden crosses, while their bearish trends begin to vanish.

A month ago, we published a report calling the market bottoms for bitcoin and ethereum. Since then, BTC and ETH have climbed 22% and 17%, respectively. Now that January’s digital asset rally has passed, we can examine the impact it had on long-term technical indicators to determine where these assets might be heading next.

Bitcoin crossed above its 50-SMA on January 4, its 100-SMA on January 12, and its 200-SMA on January 13. The 50-SMA ascended above the 100-SMA on January 25 and the 200-SMA on February 6. The 50-SMA’s cross above the 200-SMA materialized a golden cross on the daily chart. Over the last decade, roughly, golden crosses have foreshadowed positive returns.

Early Crypto adopters practically begged others to come on board — and! They mostly got rebuffed as geeks with yet another dodgy technology. Based on the initial reception, the expectation was for it to fizzle out in no time; instead, the space began to grow slowly and steadily as more and more people became enthusiasts. Even some celebrities that invested in Crypto early did so years after the first Bitcoin transaction.

Clearly, this is 2022; the Crypto market is now an internet frenzy. Many who missed out in the early days are now investing in cryptos instead of just wishing they’d joined sooner.

Below are some of the celebrities that invested in Crypto.

Reese Witherspoon

Reese Witherspoon and Crypto

Coming off the back of her media company sale, American actress Reese Witherspoon had a lot of cash to invest in other ventures.

Consequently, she announced her first Ethereum purchase on Twitter in early January 2022. Before that, she had posted a few tweets in support of Crypto and blockchain developers.

Reese is also a major backer of the World of Women NFT collection, as she promotes it frequently on her Twitter page. She’s thrown her weight behind the metaverse, too, calling for people to get ready before they are left behind.

Maisie Williams

Maisie Williams and Crypto

She is known as Arya Stark in the colossal HBO medieval television series, Game of Thrones. The English actress’ lead role in the hugely successful series catapulted her career several steps into the pinnacle of TV fame.

Maisie Williams engaged her Twitter followers in November 2020, asking them which is better between going long or short on Bitcoin. And of course, many skeptics advised her not to jump on the “bandwagon.” She bought it anyway; she announced later to thank her fans for the advice.

Lionel Messi

Messi and Crypto

Besides getting paid a significant portion of his sign-on fee in fan token $PSG, Messi also backed a blockchain-based operating system.

In addition, Messi invested in the new trend in NFT, the metaverse. His first authenticated NFT called Messiverse went live in August 2021.

Paris Hilton

Paris Hilton and Crypto

One of America’s most famous faces, Paris Hilton, is heiress to the famed Hilton family. Paris Hilton, regarded as an all-rounder in the entertainment industry, is an actress, singer, DJ, model, socialite, and businesswoman.

According to Paris in an interview with CNBC in 2021, she became an investor in Crypto long before the boom. Although she didn’t specify the exact time, some online speculators put the timeline between 2015 and 2018. She also got into NFT in 2020 before the boom.

Mike Tyson

Mike Tyson and Crypto

Mike Tyson is one of the first celebrities to get involved with Crypto. In 2015, “Iron Mike” partnered with Bitcoin ATM manufacturers “Bitcoin Direct.” The partnership got his iconic face tattoo engraved on the ATMs.

Besides his investment in Solana, his NFT collection, “Iron Mike,” is also an investor in the Cool Cats NFT collection.

Jay-Z

Jay-Z and Crypto

Jay-Z is not in crypto for fun. His series of investments made through his investment company Marcy Ventures Partners (MVP) touches different facets of Crypto. Jay-Z’s Crypto investment portfolio includes Alchemy, Ledger, and spatial LABS (sLABS).

That’s not all; Jay-Z also funded a trust with an initial investment of 500 Bitcoins in partnership with Jack Dorsey, Square CEO. The trust is to fund Bitcoin development in Africa and India. His love for NFTs has also seen him participate in the Series A funding of NFT marketplace Bitski. A fan of NFTs, he’s also a holder of some NFTs, including Cryptopunks and RTFKT Clone X.

To Cap it all, Jay-Z sits on the board of Square, which intends to build a decentralized exchange for Bitcoin.

Elon Musk

Elon Musk and Crypto

Unarguably the biggest Crypto influencer. Elon Musk, an innovative entrepreneur and current world’s richest man, built an enviable reputation as a major force influencing the rise and fall of the market, particularly Dogecoin, through his tweets and actions.

Although it’s not clear the volume of Crypto Elon musk has, what is certain is that he has at least 0.25 Bitcoin, which was gifted to him by a friend a few years ago. However, his company, Tesla, has invested $1.5 billion in Bitcoin. Tesla also started accepting Bitcoin as a means of payment in 2021.

Jimmy Fallon

Jimmy Fallon and Crypto

The host of Tonight Show, Jimmy Fallon, caught the NFT fever. He revealed in a chat with the world’s most successful NFT artist, Beeple, that he bought “an ape,” referring to a collection from the Bored Ape Yacht Club (BAYC) NFT collections through MoonPay.

Expectedly, the revelation turned into an internet frenzy in no time as many NFT enthusiasts rushed to Opensea to see the exact NFT the show host bought.

Snoop Dogg

Snoop Dogg and Crypto

Snoop Dogg is one of the few celebrities who got involved with Crypto early. In 2013, he made Bitcoin a means of payment for his new album. A unit of the album was made available for 0.3 Bitcoin each, equivalent to about $11,000 an album in today’s Bitcoin valuation.

It is unclear how much Snoop Dogg raked in from the venture or the current value of his portfolio.

He’s a holder of Bitcoin, Dogecoin, and other cryptos. His NFT portfolio includes Cryptopunks, Cool Cats, Sandbox, and other NFT collections, and he has continuously reiterated his belief in cryptocurrencies.

Mark Cuban

Mark Cuban and Crypto

Billionaire investor Mark Cuban is a businessman, TV star, and media mogul popularly known for the Shark Tank series.

The billionaire invested in several coins in the early days of Coinbase. He also has a massive investment in NFTs, and he has one of the largest NFTs portfolios as a collector.

Recently, Mark Cuban claimed 80% of his investment outside Shark Tank is in Crypto, including UniKoinGold.

Furthermore, his NBA franchise, Dallas Mavericks, started accepting payments for tickets in Bitcoin through BitPay in 2019.

Ashton Kutcher

Ashton Kutcher and Crypto

Making an unexpected turn from a red-hot acting career to focus on investing, Ashton’s foray into investment has yielded positive results so far.

His investment journey wasn’t overnight; Ashton founded the investment company “A-Grade” in 2010 with his friends. The aim was to invest in tech startup companies.

Besides investments in established tech companies like Uber and Airbnb, Ashton has also invested in a couple of Crypto startups, including BitPay and UniKoinGold, alongside billionaire Mark Cuban.

Serena Williams

Serena Williams and Crypto

It took many by surprise when news filtered that the world-famous tennis star and 23 grand slam titles winner owns a venture capital firm.

Her venture capital firm, Serena Capital, announced an investment in Coinbase in 2019 but dropped it later. Serena Ventures, however, still maintains an investment in “Cointracker,” a Crypto investment and tax tracker.

Floyd Mayweather Jr

Floyd Mayweather and Crypto

Sometime in 2017, the world’s greatest welterweight boxer posted a picture of him brandishing a card with the caption saying he was spending Bitcoin, Ethereum, and other types of cryptocurrencies in Beverly Hills on his Facebook and Twitter pages.

In retrospect, the widely accepted belief is that the post was a means of announcing he had invested in different cryptocurrencies.

Shortly after, Mayweather’s involvement with Crypto became more pronounced as he promoted the ICO of Stox $STX on his Instagram page, touting his investment in the coin.

Tom Brady

Tom Brady and Crypto

Tom Brady once stated in an interview that he wishes part of his buccaneers’ salary is paid in Crypto — highlighting his interest in the Crypto ecosystem.

Clearly, the popular Crypto exchange and one of the biggest globally, FTX, got the memo and approached Tom with a multi-million-dollar partnership deal.

Tom is also the co-founder of the NFT platform, Autograph.io.

World number 1 and four-times single grand slam winner claimed in an interview with financial magazine Bloomberg that the rise and the internet buzz around Dogecoin did catch her attention.

Subsequently, Naomi dived into the NFT pool through a joint project with her sister, Mari Osaka. The athlete’s signed projects are on the Autograph NFT platform.

Gwyneth Paltrow has a long history in lifestyle and investment advisory; this she does through “Goop,” a lifestyle brand she owns. She also joined Abra in 2017 to become the face and advisor to the Crypto wallet.

Along with other investors, Gwyneth invested in the Crypto mining operation “Terawulf” in December 2021. Terawulf is involved in a 100% zero-carbon Bitcoin mining operation, according to the CEO, Paul Prager.

The Winklevoss Brothers

The Winklevoss brothers and Crypto

Twin brothers and former US rowing team Olympians, popularly known for suing Facebook founder Mark Zuckerberg, in a claim that he stole the social network idea from them while they were in Harvard together.

The twin brothers got $65 million as part of the settlement from the suit, and they invested a significant chunk of it in Bitcoin early in 2013. Consequently, the explosion of the Crypto market saw them become the world’s first celebrity crypto billionaires.

Now, the brothers are principal shareholders in Crypto exchange Gemini, and both own an estimated 70,000 Bitcoin and other cryptocurrencies.

Founder and CEO of fintech company Square, the former CEO of Twitter, is one of the most prominent pro-Bitcoin voices globally. Jack became heavily interested in Bitcoin in 2017 and has been a significant voice in the Bitcoin crusade. An avid advocate of “buy the dip,” he indicated that he spends several thousand every week to buy Bitcoin in an interview in 2020.

Apart from his personal Bitcoin holdings, Jack’s Square is a significant investor in Bitcoin after buying a combined 4,709 Bitcoins in October 2020. In late 2021, Jack stepped down as Twitter CEO to head Square himself.

The British business mogul, the founder of Virgin Group, is known for two things: his business acumen and record-setting fun exploits.

Richard Branson participated in a $30 million funding round of the Bitcoin-based payment processing platform, BitPay. The value of his investment in the company is, however, not public. Still, if his audacious business moves are anything to go by, his investment in BitPay is expected to be significant.

NFL offensive tackle was one of the most vocal and consistent pro-Bitcoin voices in sports. In December 2020, he famously asked to be paid half of his $13 million salary in Bitcoin.

However, it didn’t take long before his wish became a reality through the Bitcoin paycheck solution “Strike.” Russell made this known on his Twitter account when he tweeted, “Got paid in Bitcoin.”

The $6.5 million received in Bitcoin, which represented half of $13 million, soon increased in value exponentially with the rise of the king cryptocurrency.

Traditional social products are often considered fully packaged content feeds and communication apps. At their core, however, they are primarily identity products. They provide the foundational connection between a person’s digital persona and their data, content, and social connections. The person-to-content linkage is foundational to digital communication and yet, it is monopolized, monetized, and manipulated via sugary feeds built by a select few closed platforms.

Decentralized Social (DeSoc) protocols are re-architecting digital identity to be user-owned and governed. With DeSoc, users are free to trustfully communicate and construct applications without manipulation or censorship for profit’s sake. Before this can happen, DeSoc networks need to achieve a minimal level of network size and overcome the current centralized platform paradigm.

The traditional social platforms have been nearly impenetrable competitively due to advantages gained by closing external access to the rich sea of profile and content relationship data known as the social graph. While profitable for the platforms, locking access to the social graph creates three core problems for creators and tangential businesses:

• Disjointed creator monetization — Creators often are forced to use tools like email lists, blogs, and partnerships in addition to social media in order to adequately monetize their content. While the total creator market grew from approximately $14 billion in 2021 to over $100 billion in 2022, creator earnings are limited due to the added user friction of having to convert across tools and platforms.

• Disproportionate platform value share — While over $230 billion is earned by social platforms largely from advertising, content creators are only earning roughly $6.5 billion in revenue share. For example, on YouTube, which has by far the most generous revenue share, nearly 98% of creators would not meet the poverty line in the US on advertising revenue share alone.

• Concentrated creator revenue distribution — Because social algorithms are optimized for predictable viewership, only the uppermost creators with predictable appeal earn the vast majority of advertising revenue. Without developer access to the social graph data, there is no subsequent business model innovation that would support a creator middle class.

Given the large revenue imbalance between platforms and creators, there is a significant incentive for technologies to bridge the gap and for creators to adopt them. With an open social graph anyone can build upon, DeSoc poses a viable threat to incumbent social platforms whose competitive moat arises from their closed architectures.

DeSoc Architecture

DeSoc protocols, like traditional social, provide the core linkage of profiles to digital content. Profiles are typically represented as NFTs, and the content published, whether its posts, videos, or comments, is all tied to the core profile either on- or off-chain. Since all of the profile and content relationships (social graph) are open and readable by developers, anyone can build front-end applications and features on top of the social graph. This breaks apart the tech stack of traditional platforms and significantly expands the potential for innovation.

In the same way that increasing the contact surface area of two chemicals produces faster, more bountiful reactions, increasing the surface area between developers and technology multiplies the potential for new applications and features.

With the increased development surface area, numerous projects have spun up to tackle more than just the core social graph. They are building every facet of consumer applications ranging from developer infrastructure like video transcoding to features like messaging and search.

While still early, these projects are largely composable and are thus rapidly culminating toward being viable consumer application infrastructure.

Over is a World Scale, open-source, AR platform powered by Ethereum Blockchain.

Over makes it possible for users provided with a mobile device or smart glasses to live interactive augmented reality experiences customized in the real world.

Over can be defined as a new standard in augmented reality experiences by placing itself as the first content browser where the user does not choose the contents but the world submits the possible experiences based on its geographical position.

Over adopts the open-source philosophy, meaning that the entire Over community contributes to its growth, thus making the platform-independent of its creators.

Over uses the Ethereum and Polygon blockchain to decentralize all the token exchange dynamics between the users.

OVR token is a utility token based on Ethereum’s smart contract ERC-20 standard.

OVRLands are parcels stored inside a blockchain-based ledger that make up the digital layer of subdivision of our planet into hexagons.

OVRLand token is a non-fungible token based on the ERC-721 standard that also allows decentralized possession of digital assets such as OVRLands and Over Experiences, that are superimposed on reality through the eye of a mobile device or a smart glass, give life to augmented reality experiences.

OVRLands are freely tradable among users in a decentralized fashion through the use of the Over marketplace and OpenSea. OVRLand owners can decide what kind of experience the user will experience once entered into the OVRLand.

Therefore the community has complete control over OVRLands and Over Experiences.

AR experiences can range from static 3D content and interactive highly complex and hyper real scenes that make virtual content merge with the real world by engaging the user to a physical interaction with the surrounding world. So far, the system exploiting these experiences are mobile devices based on iOS and Android and Smart glasses such as Hololens, Magic Leap and AR low cost headset based on the holokit project.

Over, acting as a platform, supports the current hardware available on the market and with software integrations will support all-next generation hardware launched on the market. The platform, therefore, stands as a hardware-independent standard. The Over Experiences can be realized and published thanks to a Unity3D-based SDK and a Web Builder, community users can undertake buying and selling experiences inside the platform.

Unity3D, among the leading real time 3D development environments on the market, has been chosen for its versatility, diffusion, and ability to manage a cross-platform compilation of projects thus supporting mobile devices and smart glasses.

Over implements a decentralized publishing system based on publisher/advertiser principle where the Over Owner can earn OVR token by inserting the sponsored content proposed by advertisers into the augmented reality experience.

Over is unstoppable because once implemented in the blockchain, no one will have the power to change the software rules, the OVRLand contents, and the crypto token economy.

The moderation activity will be managed by the community itself through a DAO with a reporting system with the management of blacklists maintained by the nodes.

Over is focused on the rapid growth of the mobile AR and Smart Glasses sector and introduces the following main innovations:

Development of a decentralized and unstoppable open-source platform managed by the community with its own coin and its own ecosystem.

Buying and selling digital assets (lands, contents, advertising) with the OVR utility token

Development of a combined tracking system that uses GPS, computer vision algorithms, and the inertial system onboard the device to bring the user experience to a new state of the art of outdoor and indoor AR.

The use of the IPFS* like protocol to decentralize the storage of 2D/3D assets by making the entire platform unstoppable and independent and remunerating the nodes that share their storage space and bandwhidth

Decentralization and community-powered ecosystem

Over, as you will realize in the following paragraphs, is disruptive for different sectors in addition to augmented reality such as:

In modern finance, it’s standard practice for service providers like banks to retain custody of your assets. This means, for example, that when you want to make a withdrawal from your bank account, while you may have a legal claim to the money, the reality is that you’re asking for permission from your bank. Banks can and regularly do deny such permission, and their reasons for doing so do not always align with the best interests of individual customers. Further, even when service providers uphold the custody rights of their customers in good faith, factors outside of their control may force them to deny you access to your money. For example, a government may force banks to restrict withdrawals in an attempt to stop runaway inflation, as happened in Greece in 2015. Another, perhaps more insidious example, is Operation Choke Point, where the US government pressured banks to deny service to people involved in a variety of (legal) industries it had identified as morally corrupt.

With the advent of blockchain-supported decentralized systems – of which Bitcoin is the primary example – it became possible, for the first time, to provide self-custodial financial services at a large scale. In the self-custodial model, the customer retains full custody (possession) of their assets at all times, using the service provider merely as an interface for conveniently managing their assets.

When you use a self-custodial wallet (like the Bitcoin.com Wallet), first of all, you don’t need to ask for permission to use the service. There’s no account approval process, meaning anyone in the world can download the app and start using it immediately. Secondly, only you have access to your funds. This makes it nearly impossible for the service provider (in our case Bitcoin.com), a government, or anyone else to prevent you from using your funds exactly as you wish.

Of course, with great power comes great responsibility! Since you’re the only one with access to your funds, you need to manage your wallet carefully. This includes backing up your wallet and adhering to password management best practices.

What’s the difference between self-custodial and non-custodial?

Nothing. Self-custodial == non-custodial.

Are all cryptocurrency wallets self-custodial?

Absolutely not. Centralized cryptocurrency exchanges (Coinbase, Binance, etc.) provide custodial cryptocurrency wallets (sometimes known as ‘web wallets’). While such exchanges are useful for buying, selling, and trading cryptoassets, when you use these exchanges, your crypto is held in trust by the exchange. Note that with self-custodial wallets like the Bitcoin.com Wallet, you can also buy, sell, and trade cryptocurrencies.

What are the risks associated with custodial cryptocurrency wallets?

The risks are similar to (and in many cases greater than) those associated with holding your money at a bank or using a payment app like PayPal. The risks stem from the fact that, fundamentally, you’re not in full control of your funds.

Firstly, you are exposed to the risk that the exchange will go bankrupt. If that happens, it is highly unlikely that you will recover the crypto you held on the exchange.

Second, since taking custody of financial assets is a regulated activity, centralized cryptocurrency exchanges are subject to the whims of regulators in the jurisdiction they are domiciled. And since cryptocurrency regulations are in a state of flux in most regions, this means there’s always the possibility that you’ll wake up to find you are unable to access your cryptoassets.

Next, the exchange may charge extra fees for withdrawals (which is common), slow down your withdrawal process (also common), or prevent you from withdrawing altogether (rare but not impossible).

Finally, there’s the risk that the get hacked. And since cryptocurrency exchanges generally aren’t insured and are often registered offshore, it’s likely you’ll lose your cryptoassets and have no recourse to action.

Are there any other reasons to use a self-custodial wallet?

Self-custodial crypto wallets provide you with direct access to public blockchains. The best wallets, like the Bitcoin.com Wallet, allow you customize the fees you pay to public blockchain miners and validators. This means, for example, that you can choose to pay less for transactions when you’re not in a hurry (or more if you’re in a rush!). Finally, because self-custodial wallets provide direct access to blockchains, they also enable you to interact with smart contracts. That means, for example, you can access decentralized finance products that enable you to earn passive income.

How do I know if I’m using a self-custodial wallet?

All self-custodial crypto wallets enable you (and only you) to possess the private key associated with your public address. This typically takes the form of either a file or a ‘mnemonic phrase’ that consists of 12-24 randomly generated words. If your wallet doesn’t have this option, it’s custodial (meaning you’re not in full control of your cryptoassets).

The Bitcoin.com Wallet, which is fully self-custodial, also offers a cloud backup service (in addition to giving you the option to store the private key for each of your wallets as a mnemonic phrase). With the cloud backup service, you create a single custom password that decrypts a file stored in your Google Drive or Apple iCloud account. If you lose access to your device, simply reinstall the Wallet app on a new device, enter your password, and you’ll again have access to all of your cryptoassets. Further, whenever you add more wallets within your Bitcoin.com Wallet, your backup file will automatically sync. This means you never have to worry about creating or managing a new backup for each new wallet you create!

Custodial vs. Self-custodial Wallets

Self-custody wallets tips

Only download a wallet application from the official app store or website in order to avoid fake or modified phishing versions.

Ensure your wallet devices are always updated to the latest official firmware or software available.

Always keep your recovery seed phrase or private key safe from third parties and environmental hazards such as fire and water.

Never generate or store a digital copy of your recovery seed or private key. Even your printer could keep a digital copy. Write it down instead.

Use 2 factor-authentication (2FA) and biometric verification (fingerprints, patterns etc) on your phone or laptop if you have a software wallet or use a hardware wallet application.

Be careful which smart contracts or Dapps you interact with, and avoid blind signing where possible.

If you set up 2-Step Verification, you can use the Google Authenticator app to receive codes. You can still receive codes without internet connection or mobile service. Learn more about 2-Step Verification.

1- Android

App requirements

To use Google Authenticator on your Android device, you need:

In the Authenticator app, tap More Transfer accounts Export accounts.

Select the accounts you want to transfer to your new phone. Then, tap Next. If you transfer more than one account, your old phone may create more than one QR code.

On your new phone, tap Scan QR code.

After you scan your QR codes, you get confirmation that your Authenticator accounts transferred.

Tip: If your camera can’t scan the QR code, there may be too much information. Try to export again with fewer accounts.

If you already have Authenticator for your account, remove that account from Authenticator.

Important: Before you remove an account from Authenticator, make sure you have a backup. Learn more about backup codes.

To set up 2-Step Verification for the Authenticator app, follow the steps on screen. Use the same QR code or secret key on each of your devices. Learn more about 2-Step Verification.

To check that the code or key works, make sure the verification codes on every device are the same.

2- iPhone & iPad (iOS)

App requirements

To use Google Authenticator on your iPhone, iPod Touch, or iPad, you need:

In the Authenticator app, tap More Export accountsContinue.

Select the accounts you want to transfer to your new phone, then tap Export.

If you transfer multiple accounts, your old phone may create more than one QR code.

On your new phone, tap Scan QR code.

After you scan your QR codes, you get a confirmation that your Google Authenticator accounts transferred. You can remove your exported accounts from your old phone.

Tip: If your camera can’t scan the QR code, it may be that there’s too much info. Try to export again with fewer accounts.

If you already have Authenticator for your account, remove that account from Authenticator.

Important: Before you remove an account from Authenticator, make sure you have a backup. Learn more about backup codes.

To set up 2-Step Verification for the Authenticator app, follow the steps on screen. Use the same QR code or secret key on each of your devices. Learn more about 2-Step Verification.

To check that the code or key works, make sure the verification codes on every device are the same.

Set up an authenticator app as a two-step verification method

You can set up an authenticator app to send a notification to your mobile device or to send you a verification code as your security verification method. You aren’t required to use the Microsoft Authenticator app, and you can select a different app during the set up process. However, this article uses the Microsoft Authenticator app.

Important: Before you can add your account, you must download and install the Microsoft Authenticator app. If you haven’t done that yet, follow the steps in the Download and install the app article.

Note: If the Mobile app option is grayed out, it’s possible that your organization doesn’t allow you to use an authentication app for verification. In this case, you’ll need to select another method or contact your administrator for more help.

Set up the Microsoft Authenticator app to send notifications

Select Receive notifications for verification from the How do you want to use the mobile app area, and then select Set up.

The Configure mobile app page appears.

Open the Microsoft Authenticator app, select Add account from the Customize and control icon in the upper-right, and then select Work or school account.

Note: If you receive a prompt asking whether to allow the app to access your camera (iOS) or to allow the app to take pictures and record video (Android). select Allow so the authenticator app can access your camera to take a picture of the QR code in the next step. If you don’t allow the camera, you can still set up the authenticator app as described in Manually add an account to the app.

Use your device’s camera to scan the QR code from the Configure mobile app screen on your computer, and then choose Next.

Return to your computer and the Additional security verification page, make sure you get the message that says your configuration was successful, and then select Next. The authenticator app will send a notification to your mobile device as a test.

On your mobile device, select Approve.

On your computer, add your mobile device phone number to the Step 3: In case you lose access to the mobile app area, and then select Next. Microsoft recommends adding your mobile device phone number to act as a backup if you’re unable to access or use the mobile app for any reason.

From the Step 4: Keep using your existing applications area, copy the provided app password and paste it somewhere safe.

Note: For information about how to use the app password with your older apps, see Manage app passwords. You only need to use app passwords if you’re continuing to use older apps that don’t support two-factor verification.

Select Done.

Set up the Microsoft Authenticator app to use verification codes

On the Additional security verification page, select Mobile app from Step 1: How should we contact you?.

Select Use verification code from the How do you want to use the mobile app area, and then select Set up.

The Configure mobile app page appears.

Open the Microsoft Authenticator app, select Add account from the Customize and control icon in the upper-right, and then select Work or school account.

Note: If you receive a prompt asking whether to allow the app to access your camera (iOS) or to allow the app to take pictures and record video (Android). select Allow so the authenticator app can access your camera to take a picture of the QR code in the next step. If you don’t allow the camera, you can still set up the authenticator app as described in Manually add an account to the app.

Use your device’s camera to scan the QR code from the Configure mobile app screen on your computer, and then choose Next.

Return to your computer and the Additional security verification page, make sure you get the message that says your configuration was successful, and then select Next. The authenticator app asks for a verification code as a test.

From the Microsoft Authenticator app, scroll down to your work or school account, copy and paste the 6-digit code from the app into the Step 2: Enter the verification code from the mobile app box on your computer, and then select Verify.

On your computer, add your mobile device phone number to the Step 3: In case you lose access to the mobile app area, and then select Next. Microsoft recommends adding your mobile device phone number to act as a backup if you’re unable to access or use the mobile app for any reason.

From the Step 4: Keep using your existing applications area, copy the provided app password and paste it somewhere safe.

Note: For information about how to use the app password with your older apps, see Manage app passwords. You only need to use app passwords if you’re continuing to use older apps that don’t support two-factor verification.

Investors generally prefer more experienced institutions and individuals to handle their investments for them. As a result, one of the biggest markets in the traditional finance world is the asset management industry. As of 2021, there are approximately $112.3 trillion in global assets under management (AUM). With global wealth at $463.6 trillion, approximately 24.2% of all wealth is managed by the global asset management industry.

By comparison, the asset management industry for decentralized finance (DeFi) is quite small. Altogether, the decentralized asset management (Yield Aggregator and Indexes) has a total value locked (TVL) of $1.3 billion. Given that the total market cap of all of crypto is ~$909 billion, only about 0.15% of all crypto wealth is managed through decentralized asset management. In other words, decentralized asset management’s share of wealth is ~161x smaller than traditional finance’s share of wealth.

Although decentralized asset management is lagging far behind its traditional finance counterpart, there is certainly an investor base that wants exposure to DeFi and its yield. That investor base was previously serviced by a plethora of CeFi companies, such as Celsius, Voyager, BlockFi, etc., that gained popularity over the 2021 bull run. Part of their popularity was due to their relatively simple and convenient interfaces. However easy-to-use these CeFi solutions were, they came with some complications in regard to their opaqueness and custodial nature.

Decentralized asset management may stand to benefit from CeFi’s failure. The recent FTX implosion has evaporated the trust of many users in centralized custodians. As such, decentralized non-custodial solutions are necessary to help regain the trust of so many that were negatively affected by FTX. In decentralized asset management, users don’t have to worry about a custodian losing their crypto. Moreover, users can verify, on-chain, the health of the products they choose to invest their money in.

Although decentralized finance’s asset management industry may be small, numerous protocols and projects are working to scale the nascent industry. Enzyme is leading the charge as the largest on-chain active asset management platform by TVL.

Background

The private company behind Enzyme, Melonport AG, was founded in July 2016 as a privately domiciled company in Switzerland. Its founders, Mona El Isa and Reto Trinkler, aimed to develop an asset management protocol on Ethereum called Melon, the predecessor name for Enzyme.

Melon V1 went live in March 2019. It allowed users to create and invest in crypto structures through the use of smart contracts. Upon the launch of Melon V1, Melonport AG wound down and handed control of the Melon protocol to the community through the Melon Council, in an effort to decentralize the project. The Melon Council was a governing body initially selected by Melonport AG prior to its dissolution.

In December 2020, Melon Protocol announced that it would be rebranding to Enzyme. The Melon Council was additionally rebranded to the Enzyme Council. On Jan. 21, 2021, Enzyme V2 introduced new smart contract architecture and enabled new features such as lending and synthetic assets. In Q1 2022, Enzyme launched the latest release, Sulu, and deployed the protocol on Polygon.

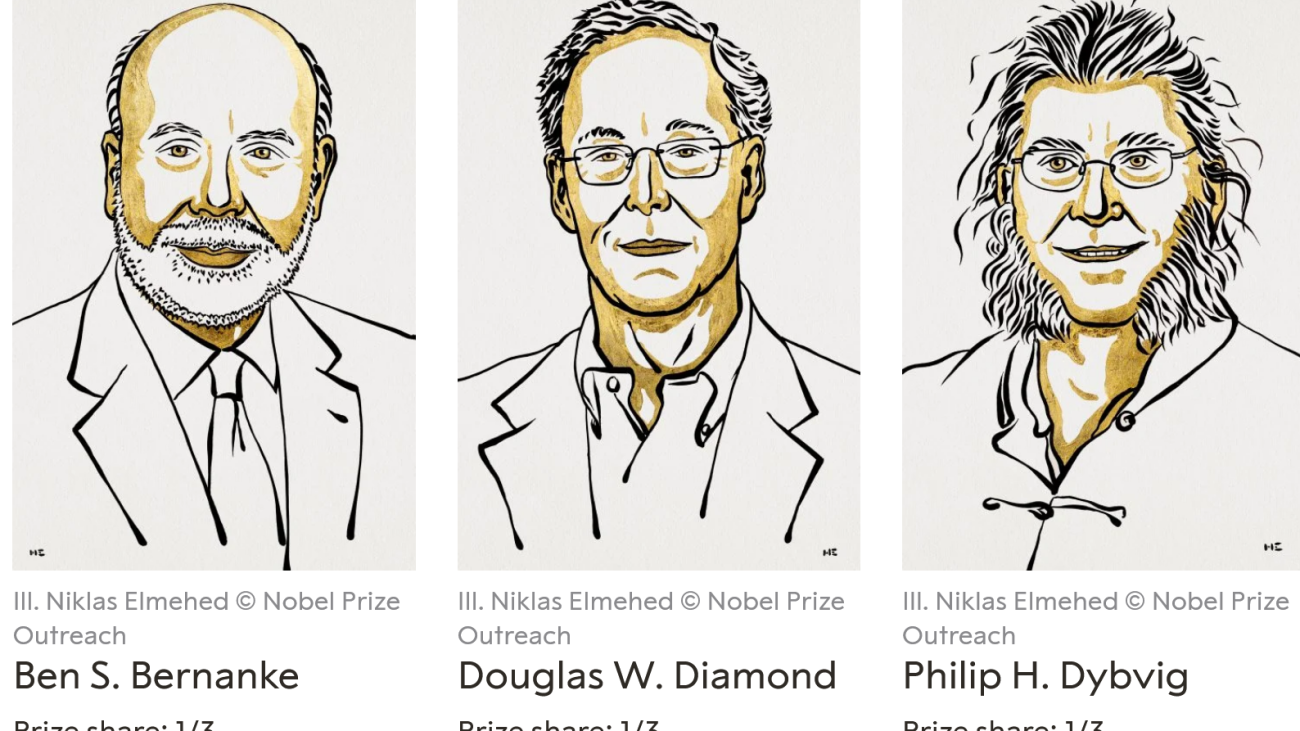

The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2022 was awarded jointly to Ben S. Bernanke, Douglas W. Diamond and Philip H. Dybvig “for research on banks and financial crises” explained briefly below:What is the role of banks in the economy and society? What happens if they collapse?

The foundations of modern banking research were laid by Ben Bernanke, Douglas Diamond and Philip Dybvig in the early 1980s. Through statistical analysis and historical source research, Bernanke demonstrated how failing banks played a decisive role in the global depression of the 1930s. Bernanke’s research shows that bank crises can potentially have catastrophic consequences. This insight illustrates the importance of well-functioning bank regulation.

Ben Bernanke

Ben S. Bernanke – Nobel Prize in Economic Sciences

A rug pull is a type of crypto scam that occurs when a team pumps their project’s token before disappearing with the funds, leaving their investors with a valueless asset.

Rug pulls happen when fraudulent developers create a new crypto token, pump up the price and then pull as much value out of them as possible before abandoning them as their price drops to zero. Rug pulls are a type of exit scam and a decentralized finance (DeFi) exploit.

Before learning how to spot a rug pull in crypto and why crypto rug pulls happen, it helps to understand the three different types of rug pulls.

2.

What are the various types of rug pulls?

There are three main types of rug pulls in crypto: liquidity stealing, limiting sell orders and dumping.

What are the various types of rug pulls?

Liquidity stealing occurs when token creators withdraw all the coins from the liquidity pool. Doing so removes all the value injected into the currency by investors, driving its price down to zero.

These “liquidity pulls” usually happen in DeFi environments. A DeFi rug pull is the most common exit scam.

Limiting sell orders is a subtle way for a malicious developer to defraud investors. In this situation, the developer codes the tokens so that they’re the only party that is able to sell them.

Developers then wait for retail investors to buy into their new crypto using paired currencies. Paired currencies are two currencies that have been paired for trading, with one against the other. Once there is enough positive price action, they dump their positions and leave a worthless token in their wake.

Dumping occurs when developers quickly sell off their own large supply of tokens. Doing so drives down the price of the coin and leaves remaining investors holding worthless tokens. “Dumping” usually occurs after heavy promotion on social media platforms. The resulting spike and sell-off are known as a Pump-and-Dump Scheme.

Dumping is more of an ethical gray area than other DeFi rug pull scams. In general, it’s not unethical for crypto developers to buy and sell their own currency. “Dumping,” when it comes to DeFi cryptocurrency rug pulls, is a question of how much and how quickly a coin is sold.

3.

Hard pulls vs soft pulls

Rug pulls come in two forms: hard and soft. Malicious code and liquidity stealing are hard pulls, whereas soft pulls refer to dumping an asset.

Rug pulls can be “hard” or “soft.” Hard rug pulls occur when project developers code malicious backdoors into their token. Malicious backdoors are hidden exploits that have been coded into the project’s smart contract by the developers. The intent to commit fraud is clear from the get-go. Liquidity stealing is also considered a hard pull.

Soft rug pulls refer to token developers dumping their crypto assets quickly. Doing so leaves a severely devalued token in the hands of the remaining crypto investors. While dumping is unethical, it may not be a criminal act in the same way that hard pulls are.

4.

Are crypto rug pulls illegal?

Crypto rug pulls are not always illegal, but they are always unethical.

Hard rug pulls are illegal. Soft rug pulls are unethical, but not always illegal. For example, if a crypto project promises to donate funds but chooses to keep the money instead, that’s unethical but not illegal. Either way, like most fraudulent activities in the crypto industry, both types can be challenging to track and prosecute.

The collapse of the Turkish cryptocurrency exchange Thodex is a prime example of a rug pull in crypto. The $2 billion dollar theft was one of the biggest crypto rug pulls of 2021. It is also one of the largest centralized finance (CeFi) exit scams in history.

Although Turkish police detained 62 people during its investigation of the major scam, the whereabouts of the alleged perpetrator remains unknown.

There are several clear signs that investors can watch out for to protect themselves from rug pulls such as the liquidity not being locked and no external audit having been conducted.

The following are six signs users should watch out for to protect their assets from crypto rug pulls.

Unknown or anonymous developers

Investors should consider the credibility of the people behind new crypto projects. Are the developers and promoters known in the crypto community? What is their track record? If the development team has been doxxed but isn’t well known, do they still appear legitimate and able to deliver on their promises?

Investors should be skeptical of new and easily faked social media accounts and profiles. The quality of the project’s white paper, website, and other media should offer clues about the project’s overall legitimacy.

Anonymous project developers could be a red flag. While it’s true that the world’s original and largest cryptocurrency was developed by Satoshi Nakamoto, who remains anonymous to this day, times are changing.

No liquidity locked

One of the easiest ways to distinguish a scam coin from a legitimate cryptocurrency is to check if the currency is liquidity locked. With no liquidity lock on the token supply in place, nothing stops the project creators from running off with the entirety of the liquidity.

Liquidity is secured through time-locked smart contracts, ideally lasting three to five years from the token’s initial offering. While developers can custom-script their own time locks, third-party lockers can provide greater peace of mind.

Investors should also check the percentage of the liquidity pool that has been locked. A lock is only helpful in proportion to the amount of the liquidity pool it secures. Known as total value locked (TVL), this figure should be between 80% and 100%.

Limits on sell orders

A bad actor can code a token to restrict the selling ability of certain investors and not others. These selling restrictions are hallmark signs of a scam project.

Since selling restrictions are buried in code, it can be difficult to identify whether there is fraudulent activity. One of the ways to test this is to purchase a tiny amount of the new coin and then immediately attempt to sell it. If there are problems offloading what was just purchased, the project is likely to be a scam.

Skyrocketing price movement with limited token holders

Sudden massive swings in price for a new coin should be viewed with caution. This unfortunately rings true if the token has no liquidity locked. Substantial price spikes in new DeFi coins are often signs of the “pump” before the “dump.”

Investors skeptical about a coin’s price movement can use a block explorer to check the number of coin holders. A small number of holders makes the token susceptible to price manipulation. Signs of a small group of token holders could also mean that a few whales can dump their positions and do severe and immediate damage to the coin’s value.

Suspiciously high yields

If something sounds too good to be true, it probably is. If the yields for a new coin seem suspiciously high but it doesn’t turn out to be a rug pull, it’s likely a Ponzi scheme.

When tokens offer an annual percentage yield (APY) in the triple digits, although not necessarily indicative of a scam, these high returns usually translate to equally high risk.

No external audit

It is now standard practice for new cryptocurrencies to undergo a formal code audit process conducted by a reputable third party. One notorious example is Tether (USDT), a centralized stablecoin whose team had failed to disclose that it held non-fiat-backed assets. An audit is especially applicable for decentralized currencies, where default auditing for DeFi projects is a must.

However, potential investors shouldn’t simply take a development team’s word that an audit has taken place. The audit should be verifiable by a third party and show that nothing malicious was found in the code.

Spotting a crypto rug pull scam: It takes some digging

In 2021, an estimated $7.7 billion was stolen from investors in rug pull cryptocurrency scams. These investors trusted that they were investing in legitimate projects, only to have the rug pulled from beneath their feet.

Before investing, it’s worth taking the time to research new cryptos and to do one’s due diligence before investing in a new project.